A Better Balance: Market Review and Outlook | Pacific Wealth Planning

A Better Balance: Market Review and Outlook

The markets took investors on a turbulent ride in 2023, outperforming expectations for the better part of the year and ending on a high note. With one exception – commodities – last year turned out to be an impressive year for risk assets.

What drove the dramatic rebound? After a dismal year for stocks and bonds in 2022, investors headed into 2023 with plenty of reasons to be wary. However, as the year ran its course, many of the big issues that haunted investors dissipated.

At long last, inflation – as measured by the broad Consumer Price Index – began to cool, giving the Federal Reserve room to shift from interest-rate increases to anticipated cuts in 2024. Meanwhile, the widely predicted recession never materialized. So far, the U.S. economy has been remarkably resilient in the face of today’s higher-rate regime.

As we look down the open road of a new year, the question is whether the rally that began in 2023 will continue into this year. While there are still plenty of risks (more on this below), there are good reasons to believe the rally has staying power. Still, investment opportunities may look different this year if, as we expect, the rally broadens to sectors and smaller companies that have lagged.

Before we delve into our market outlook, here’s a recap of 2023 asset-class returns:

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Note: views are from a U.S. dollar perspective. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from FactSet. Index proxies: Bloomberg U.S. AGG Bond Index, ICE BofA U.S. Corporate, ICE BofA U.S. High Yield, S&P 500, MSCI EM, MSCI World ex US Index, Dow Jones U.S. Select REIT, and Bloomberg Commodity Index. Data as of December 29, 2023.

A Lighter Load

As we enter 2024, many investors are undoubtedly feeling a bit sunnier, and that’s not just because spring will be here before we know it.

- Although inflation remains above the Fed’s 2% target rate, the CPI has been trending in the right direction. In response, the Fed has signaled that it is not only done raising rates but could cut rates three times this year for a total of 75bps.

- In recent months, the widely followed federal funds futures market has been forecasting (perhaps a bit too bullishly) that the central bank will cut rates more aggressively (five times) this year, dropping its benchmark rate to 4.00% by year-end from 5.5% currently.

- The all-important U.S. labor market remains tight, with companies continuing to hire, albeit at a slower pace (measured by job postings) in recent months. Labor-market conditions will factor prominently into the Fed’s calculus regarding rate cuts.

- U.S. consumers have also weathered the higher-rate environment pretty well. That has a lot to do with the fact that the debt profile of households with significant amounts leverage is comprised largely of lower-rate, longer-term mortgage balances – versus higher-rate, shorter-term credit-card balances.

We’ve been saying for some time that where the fed funds rate peaks will ultimately be less important than how long it remains at that high point. If, as the market anticipates, the central bank cuts rates this year, the collateral damage of the Fed’s battle against inflation should remain limited.

But, the Fed will need to tread cautiously. If the Fed acts too slowly, the pain of prolonged high rates will surely cut deeper, particularly for Americans with large amounts of credit card debt. Interest rates on credit card debt have soared to record levels over the last couple years, and delinquencies have now surpassed pre-Covid levels. Conversely, if the Fed cuts rates too quickly, it could reignite inflation and heat up the economy, driving an increase in wage and price growth.

Credit Card Interest Rates and Delinquencies Climb

Source: Kestra Investment Management, FRED, and New York Fed Consumer Credit Panel / Equifax. Data as of November 30, 2023.

Still, some of the classic indicators that we use to gauge the probability of a recession – namely the yield curve and the ISM manufacturing index – are trending in a better direction than they were about a year ago. Back then, they were flashing warning signs, leading many (present company included) to predict that the economy was headed for a recession. On this account, we were happily wrong. While a recession is still possible, it will likely be mild and asset prices may have already priced a slowdown in. While the yield curve remains inverted, a decrease in short-term rates should help normalize the shape of the yield curve. And while the ISM manufacturing index remains in contractionary territory, it appears to be bottoming.

Signs of Bottoming in Manufacturing; Tenuous Expansion for Services Sector

Forward looking projections may not come to pass. Source: Kestra Investment Management, Institute For Supply Management and FactSet. Data as of December 29, 2023

Where do the markets go from here?

Given the positive economic backdrop and the likelihood of rate cuts, the outlook for corporate earnings, a major driver of market performance, is looking pretty good.

In early January, analysts were expecting year-over-year earnings for S&P 500 companies to grow by a robust 12% , according to FactSet. Over the course of the year, analysts are likely to dial back their expectations, as they usually do. Yet, even if earnings fall short of current expectations, we’re likely to see a decent increase in corporate profits, perhaps one approximating a more-normal growth rate of 9%-10% annually.

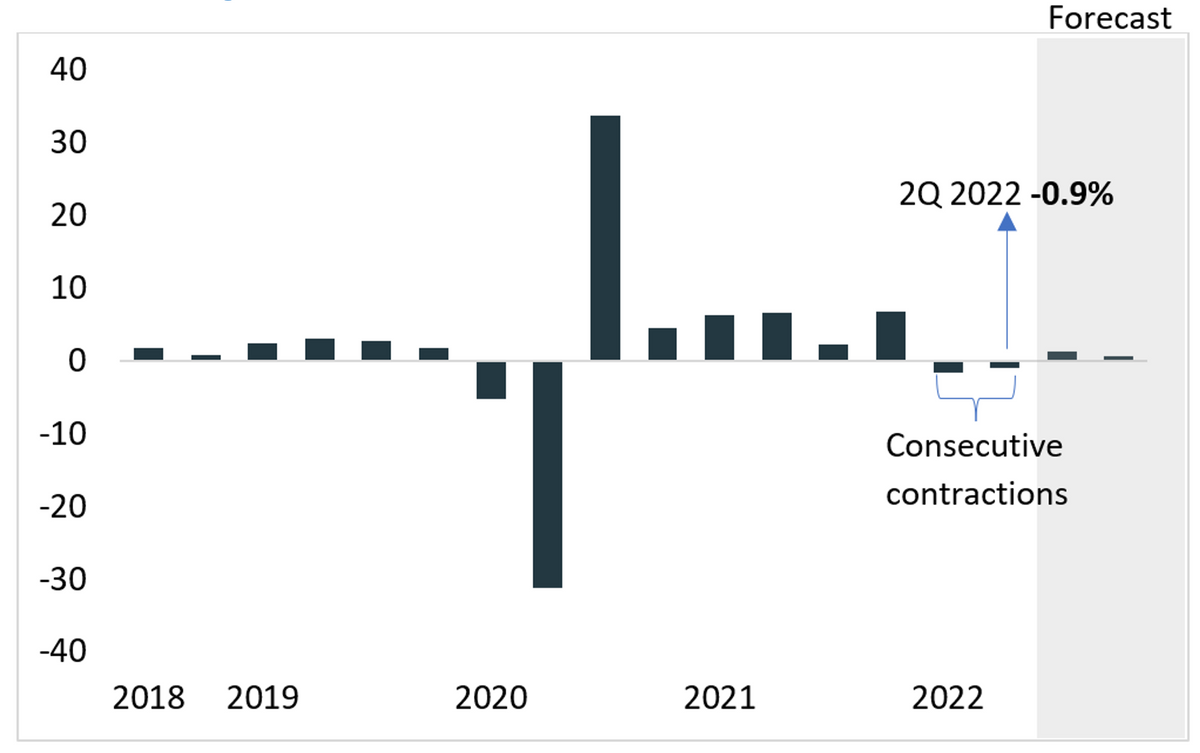

From their peak in the fourth quarter of 2021 to their trough in the second quarter of 2022, corporate earnings dropped by 14%, consistent with what we have typically seen during a mild recession. This decline might suggest that the expected economic weakness is already behind us. From here, earnings will need to kick in to help justify equity valuations that are fairly high by historical standards, as measured by 10-year average price-to-forward earnings ratios for the S&P 500.

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Note: views are from a U.S. dollar perspective. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from FactSet. Index proxies: S&P 500. Data as of December 29, 2023.

This is especially true for Technology, which went from being the worst-performing sector in 2022 to the best performing, most richly valued last year. The sector’s price-to-earnings ratio surpassed its historical average of 19 in October 2022, and it currently sits just over 26, as of year-end 2023.

The headline-grabbing promise of artificial intelligence has fueled the steep rise in the share prices of a handful of Technology stocks, helped by improved post-Covid profit margins. We believe AI will change the way we do business for the foreseeable future, and some of today’s Tech darlings stand to benefit from this sea change. That said, steeply higher valuations leave little room for error.

Where do we see opportunity this year?

After a year in which returns were driven by a very limited number of names, we believe 2024 will bring a broader set of investment opportunities.

- After lagging for some time, small- to medium-sized companies will have a chance to outperform as interest rates decline. More-defensive sectors (including Health Care, Consumer Staples, Energy and Utilities) should also benefit from the proverbial rising tide that lifts all boats.

- The fixed-income market, which rebounded in 2023, should continue to shine again this year. As of September, yields for nearly every segment of the bond market stood at multi-decade highs, which can provide attractive returns even without interest rates falling. Prices rise when yields fall and vice versa.

Note: When it comes to fixed income, we’re somewhat cautious on high-yield bonds. Based on data through November, 2023 could shape up to be the biggest year for corporate bankruptcies since 2010. Under these conditions, we’d expect high-yield bond spreads to widen. Instead, they’ve narrowed over the past 18 months, indicating the market may be failing to price in risks.

The Takeaway

Many of the worries that weighed heavily on investors last year have thankfully dissipated, but the markets and the economy still face plenty of risks, including inflation, conflict in the Middle East and Ukraine, and lofty valuations in the broader market.

The looming presidential election also adds uncertainty and will grip the nation’s attention for the better part of this year. The good news is that elections tend to have little impact on the economy and the markets over the long-term.

So, even as the rally continues into 2024, investors should expect some bumps in the road. As always, a well-diversified portfolio can help to absorb the impact, making it easier for investors to stay focused on their long-term goals.

Invest wisely and live richly,

Kara

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. Does not offer tax or legal advice.