Markets in a Minute: The R-Word -- Are We in a Recession? | Pacific Wealth Planning

Over the past few months, it’s felt like I’ve been on an extended road trip with a recession destination. Everyone from my friends, family, colleagues, and social media followers have been asking, “are we there yet?” much like my kids do when we’re on a family road trip. The truth is, we’ll get there … eventually. So, if we’re headed down the road towards the next recession, let’s use the “road signs” along the way to help us estimate when we might arrive and what we can do before we get there.

Throughout my career, I’ve leaned on two key indicators that have proven to be reliable signals of a future recession—the Treasury yield curve and the ISM Manufacturing Index. Let’s see what these indicators are telling us.

Treasury Yield Curve

We can understand a lot about the economy by looking at the Treasury yield curve and evaluating short-term yields relative to their longer-dated siblings. In essence, yield curves measure interest rates of bonds with equal credit quality but different maturity dates. In normal times, when the economy is growing, the yield curve will tend to be upward-sloping, with yields on longer maturity bonds higher than shorter-term bonds. Understandably, investors typically expect to be paid more for, say, a 10-year bond versus a 2-year bond.

But in times of trouble, this relationship changes. The Federal Reserve may start hiking short-term interest rates, as they are now, sending them above longer-term rates. Hence an inverted, downward-sloping yield curve in which shorter-term bonds carry higher yields than longer-term bonds.

To measure this relationship, we can examine 10-year Treasury yields relative to 2-year Treasury yields. When those two points are inverted for an extended period, this is a clear sign that a recession is on the horizon, but the timing can vary significantly. Since 1950, any time we have had 10-year Treasury yields above their 2-year counterparts, a recession has occurred anytime from six months to two years after the yield curve inverts.

Treasury Yield Curve Deeply Inverted

Source: Kestra Investment Management, Federal Reserve System, FactSet. Index proxies: 2 Year & 10 Year Treasury Index.

Forward looking estimates may not come to pass. Past performance is no guarantee of future results.

Data as of September 30, 2022.

In addition to simply reaching an inversion, we can examine how deeply the yield curve is inverted (i.e. how much lower is the 10-year yield relative to the 2-year) and for how long. Here’s where we’re at currently:

- The 10-year to 2-year Treasury yields have been inverted since May 7, 2022 and were recently inverted by more than 40 basis points. Relative to previous inversions, this would rank among the more severe.

- The curve has been inverted a total of 146 days. Going back to 1986, the yield curve has stayed inverted for an average duration of 256 days.

Based on both the depth and length of the current yield curve inversion, it appears clear that the economy will face a recession sometime in the future.

When Recession?

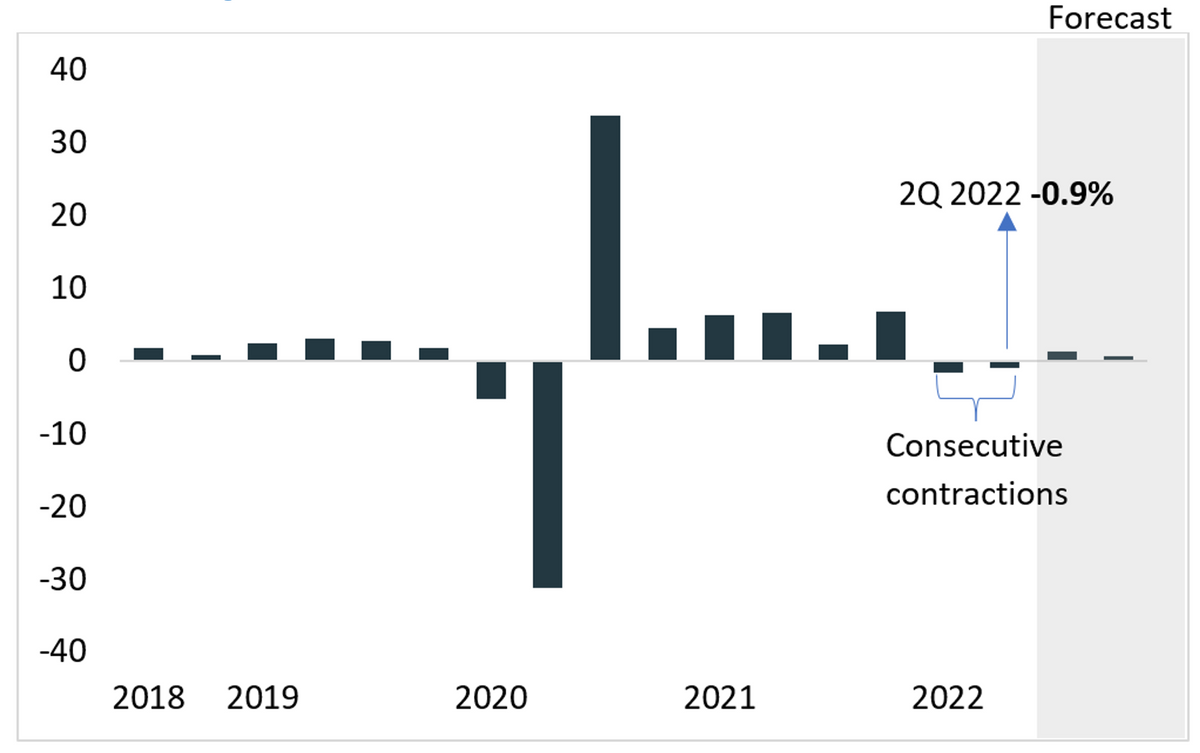

The other indicator that can help us understand the timing of entering or exiting a recession is the ISM Manufacturing Index or Purchasing Managers’ Index (PMI). This index surveys supply manufacturers on a monthly basis to give us a quick glimpse into the demand for products based on the ordering activity of manufacturers. The manufacturing industry has a solid track record of providing a leading view of overall economic conditions. The PMI is comprised of a diffusion index that summarizes whether market conditions are expanding, contracting, or staying the same:

- Anything above 50 indicates growth, and anything below means shrinking

- Historically, when the index falls below 47, there is a confirmed recession

We can peer into the future by analyzing one specific component of the PMI—New Orders. The New Orders component measures the number of new orders a company receives relative to the previous month. That number usually precedes the overall PMI by several months. New Orders briefly dipped below 50 in July for the first time since April 2020 but have since slid and are currently sitting at 47.1.

ISM Manufacturing – Not Quite in Recessionary Territory

Source: Kestra Investment Management, Institute For Supply Management and FactSet.

Data as of September 30, 2022.

If the yield curve tells us that a recession is coming, the ISM is telling us not quite yet. But if the downward momentum that we have seen over the last few months continues, it would suggest we could see an official recession by the first half of 2023.

What Should Investors Do?

Answering the question of whether a recession is on the horizon, as difficult as it may be, is easier than predicting what the market will do. Stocks have a tendency to turn down before a recession even starts and then to rebound well before it’s over. Investors who wait until the coast is clear inevitably miss accretive opportunities. It’s helpful to remember that markets go up much more often than they go down.:

- Going back to the 1960s, on average, bear markets have declined by -38% over 446 days

- By contrast, bull markets have typically risen by 209% over 2,069 days

Bear Markets Are Painful, But Shorter Lived than Bulls

Forward looking estimates may not come to pass. Past performance is no guarantee of future results.

Source: Kestra Investment Management, Charles Schwab and FactSet. Data as of April 4, 2022.

In recessionary periods, one helpful tool can be dollar cost averaging: invest a fixed dollar amount on a regular basis (weekly or monthly), regardless of the share price. If prices decline, an investor will buy more shares, potentially providing greater chances for growth in the future.

On all road trips, you’re bound to run into some bumpy roads that make the drive more stressful, uncomfortable, and uneasy. But it won’t last the whole trip. And when you think about the entire journey, those bumpy roads account for just a small fraction of your trip.

To put that into a financial perspective, as the investor and author Brian Feroldi recently said, “when in doubt, zoom out.” The S&P 500 has declined 23% so far in 2022. But over the past five years, it has returned 58% and a whopping 207% over the last ten. Recessions won’t last forever, zoom out and keep that big picture in mind when the markets make you feel uneasy.

Invest wisely and live richly,

Kara

Dollar cost averaging does not assure a profit and does not protect against a loss in declining markets. This strategy involves continuous investing; you should consider your financial ability to continue purchases no matter how prices fluctuate.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Bluespring Wealth Partners, LLC, and Grove Point Financial, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, Bluespring Wealth Partners, LLC, and Grove Point Financial, LLC. Does not offer tax or legal advice.