Finding Higher Ground: Cautiously Optimistic For 2026

Finding Higher Ground: Cautiously Optimistic For 2026

Key Takeaways

- The start of the Iran conflict and related oil shock drove the S&P 500 index to its first quarterly loss since early 2025. But some corners of the market fared better than others.

- The conflict-driven surge in oil prices has created new inflationary pressures and dampened expectations for rate cuts this year. The broad U.S. bond market was flat in the first quarter amid new headwinds for fixed income.

- The U.S. economy entered the latest Middle East crisis on pretty solid ground, which bodes well for its ability to withstand the shock, with some important caveats.

After finishing strong in 2025, the broad U.S. equities market got off to a rocky start this year. Stocks initially traded higher during the first quarter, but the onset of the Iran conflict in late February and resulting global spike in oil prices clouded the economic picture and triggered a broad selloff.

When the dust settled, the S&P 500 posted its first quarterly loss in a year (-4.3%). Does a difficult first quarter portend a down year? Not necessarily. In this week’s Markets in a Minute, we unpack first quarter performance and touch on some reasons to be cautiously optimistic about the balance of the year.

Pockets of Resilience

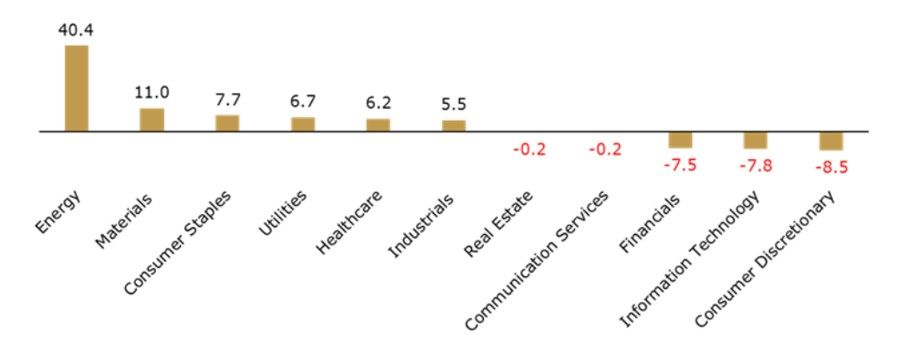

As usual, even in a down quarter, some corners of the market held up better than others. Six out of 11 S&P 500 sectors actually had positive returns for the quarter, although Energy was the clear winner.

Even before the start of the Iran conflict, energy stocks had been gaining ground, lifted by solid earnings growth tied to data-center demand and the broad sector rotation that began in late 2025. In fact, in a few areas of the market, the conflict only accelerated a trend that was already underway.

For the past several years, the market’s gains were largely driven by a small group of megacap technology stocks. Last fall, however, the landscape began to shift. Investors started looking beyond big tech for returns, resulting in more broad-based (and ultimately healthier ) market performance. Sectors such as Energy, Industrials, and Materials have been clear beneficiaries from the recent rotation.

S&P 500 Sector Performance (Oct. 2025-March 2026)

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from FactSet. Index Proxies: S&P 500 sector indexes. Data as of March 31, 2026.

Bonds Tread Water, Inflation Pressure Returns

The Iran conflict has also had ripple effects across asset classes, including the bond market. At the start of the year, the Federal Reserve was widely expected to cut its benchmark interest rate twice in 2026, which would have provided a tailwind for bonds and the broader economy. But the conflict-driven spike in oil prices led to the monthly Consumer Price Index posting its largest annual increase since May 2024 in its latest release.

Renewed concerns about inflation have dimmed the prospects for rate cuts this year and created a conundrum for the central bank. When inflation heats up, the Fed typically responds by raising rates, acting as a brake on the economy and tamping down prices. But doing so could exacerbate current softness in the labor market, which has been fluctuating between monthly job losses and gains for the past year.

On top of all this, headline-grabbing concerns about the private credit market have contributed to investor unease around fixed income. The collective headwinds have caused credit spreads to widen somewhat this year, putting a damper on fixed-income activity.

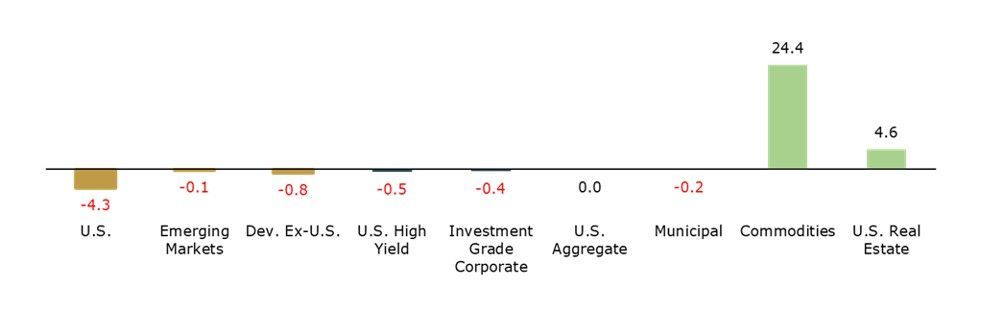

Global Market Returns, % – Q1 2026

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. Note: views are from a U.S. dollar perspective. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment Management with data from FactSet. Index proxies: Bloomberg U.S. AGG Bond Index, ICE BofA U.S. Corporate, ICE BofA U.S. High Yield, Bloomberg Municipal Bond, S&P 500, MSCI EM, MSCI World ex-U.S., Dow Jones U.S. Select REIT, and Bloomberg Commodity Index. Data as of March 31, 2026.

An Economic Tipping Point?

Over the last few years, the U.S. economy has remained remarkably resilient in the face of external shocks stemming from tariffs, geopolitical uncertainty and growing concerns about the sustainability of capital expenditures for artificial intelligence (AI), among other stressors. Could the Iran conflict mark a tipping point?

The answer remains to be seen, but there are reasons to believe the conflict’s economic damage will be fairly limited. Perhaps most importantly, the U.S. economy was on pretty solid footing before the conflict began, and nearly two months into the crisis, certain key indicators are still flashing green.

Corporate earnings, for instance, have grown by double digits for five consecutive quarters, and early reports suggest that this year’s first quarter could shape up to be the strongest earnings season in roughly five years. As of early April, S&P 500 companies were expected to report a blended (year-over-year) earnings growth rate of 13.2% for the first quarter, according to FactSet.

Manufacturing has been another bright spot this year. Manufacturing activity contracted for much of last year but has rebounded over the last few months, supported by new orders and production, according to the Institute for Supply Management’s monthly purchasing managers index.

There’s no denying that high oil prices — which act as a tax, limiting how much consumers can spend on other items — are a drag on economic growth. But we believe that the amount of time that prices remain elevated will ultimately matter more than how high they climb on any given day.

It’s also worth noting that lofty oil prices tend to have an uneven impact on consumer groups and global markets. Pain at the pump has hit lower- and middle-income households harder than those with deeper pockets. Meanwhile, regions that are heavily dependent on oil imports (namely East and South Asia and parts of Europe) have felt the sting of high prices more acutely than the United States and other markets that produce more at home.

History Lessons and Political Pressures

The conflict has already taken a tragic a human toll that shouldn’t be overlooked. At the same time, history offers some valuable context as to how markets tend to respond in the wake of major geopolitical shocks. Across decades of market data, U.S. equities have performed well in the year after major geopolitical events, with the notable exception of World War II. The S&P 500’s median return 12 months after 44 different political shocks since 1940 has been nearly 10%, according to our analysis.

This particular conflict may also prove relatively short-lived. The majority of Americans oppose the conflict, which has been costly for the government as well as households squeezed by high gas prices. Its unpopularity puts pressure on President Trump to find a politically palatable way out sooner rather than later. With the midterms coming up in November, some of that pressure may come from members of his own party.

The Bottom Line

The first quarter underscored the importance of looking past short-term noise and staying focused on the fundamentals, which remain pretty strong. Recall that the first quarter of 2025 ended on a down note, but the market subsequently rallied and finished the year up nearly 17%.

We’ve already seen the market rebound sharply in April on signs of de-escalation in the Iran conflict and earnings strength. But the situation is highly fluid and will continue to loom large until a more-durable peace takes hold.

Invest wisely and live richly

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.