Headlines are Loud, Earnings are Louder: Strong Fundamentals During Uncertain Times

Kara Murphy

Headlines are Loud, Earnings are Louder: Strong Fundamentals During Uncertain Times

- Earnings are exceeding expectations at one of the strongest rates in years, signaling broad resilience across corporate America.

- Growth is not concentrated in one area; most sectors are expanding revenues and profits at a solid pace.

- The key question now is sustainability, as markets look for companies to carry this momentum through a more uncertain global backdrop.

Despite the geopolitical uncertainty of the ongoing conflict in Iran, US companies continue to grow their earnings at impressive rates. Almost 90% of companies in the S&P 500 have reported their results for the first quarter of 2026, and 84% of them have beaten expectations through May 8th[1]. That’s higher than the 5-year and 10-year averages and the strongest quarter in nearly five years.

Estimates for year-over-year earnings growth continue moving higher, with FactSet tracking 27.5% growth for the quarter. That’s almost double what was expected at the end of March and a level that hasn’t been seen since 2021 when the economy was bouncing back from the pandemic. These results suggest the economy is thriving across many different areas.

Strength Across Sectors

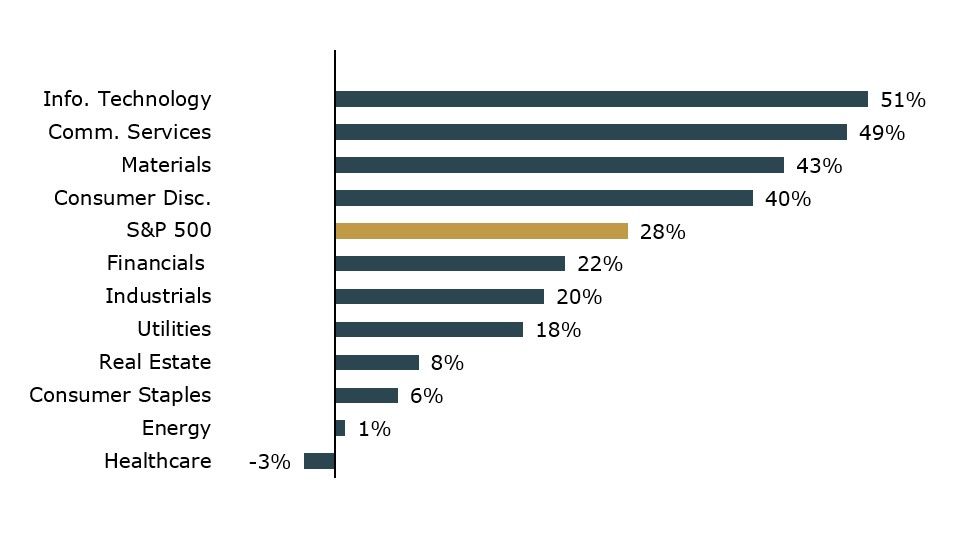

As evidence of broad-based strength of the market, seven of eleven sectors are on pace to grow earnings by double digits, while only one sector, Healthcare is expected to see earnings fall on a year-over-year basis. Information Technology, Communication Services, Consumer Discretionary, and Materials are leading the way, with all four sectors growing earnings by at least 40% this quarter.

S&P 500 Q1 2026 Year-over-Year Earnings Growth

Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast or guarantee of future results. Source: Kestra Investment with data from FactSet. Data as of May 8, 2026.

It’s not just earnings that are driving the excellent run. Net profit margin for the quarter is 14.7%, which would be the highest the index has posted since FactSet began tracking the measure in 2009. The 11.3% revenue growth rate is higher than both the 5-year and 10-year averages and would be the highest rate the index has seen since Q2 2022. All 11 sectors are growing their revenues year-over-year, with Information Technology, Communication Services, and Utilities leading the way.

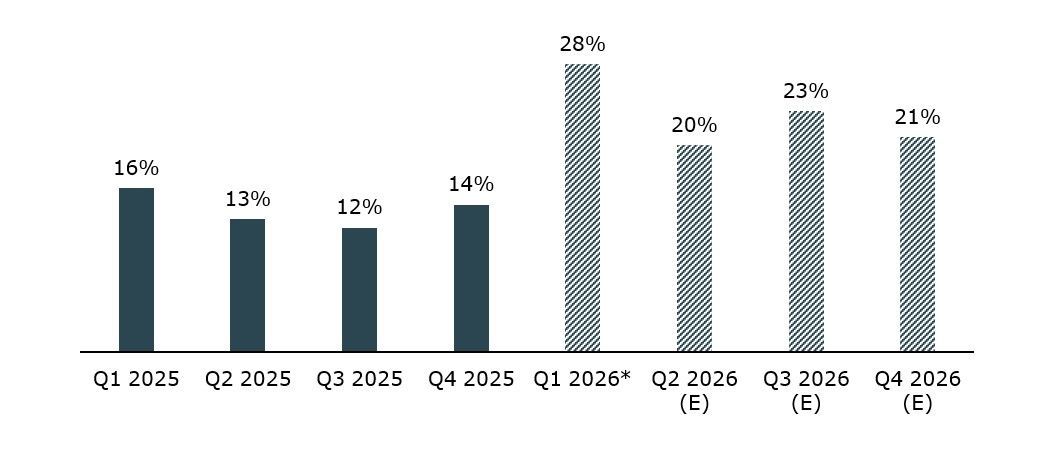

This strong pace is expected to continue through 2026 with full-year 2026 earnings growth rate for the S&P 500 is expected to reach 21%.

S&P 500 Quarterly Year-over-Year Earnings Growth: 2025 actuals and 2026 estimates

Estimates for 2026 earnings are from FactSet’s Earnings Insight. * - blended earnings growth rate based on a combination of reported earnings numbers with 90% of companies reporting and projections for the remaining companies. Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast or guarantee of futures result. Source: Kestra Investment Management with data from FactSet. Index: S&P 500. Data as of May 8, 2026.

Energy is a sector to watch moving forward. While the price of oil has risen dramatically because of geopolitical tensions and the closure of the Strait of Hormuz, Energy sector earnings have not yet benefited. While the sector posted just 1% year-over-year growth in earnings, Energy stocks have rallied in anticipation of higher earnings later in the year as price increases flow through to profits.

The Bottom Line

Strong earnings, expanding margins, and broad participation across sectors point to an economy that continues to grow, even as headlines might suggest otherwise. Markets often follow earnings over time, so the key question from here is whether companies can sustain this level of performance as costs, interest rates, and geopolitics evolve. That’s what we’ll be watching next.

Invest wisely, live richly

Kara

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.