Can U.S. Stocks Continue Earnings Momentum?

Can U.S. Stocks Continue Earnings Momentum?

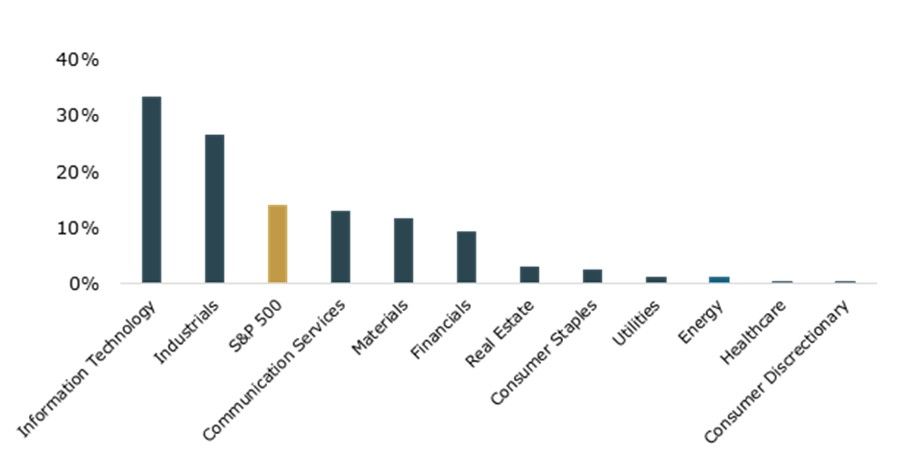

S&P 500 Q4 2025 Year-over-year Earnings Growth

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast or guarantee of futures results. Source: Kestra Investment Management with data from FactSet Earnings Insight. Index: S&P 500. Data as of February 27, 2026.

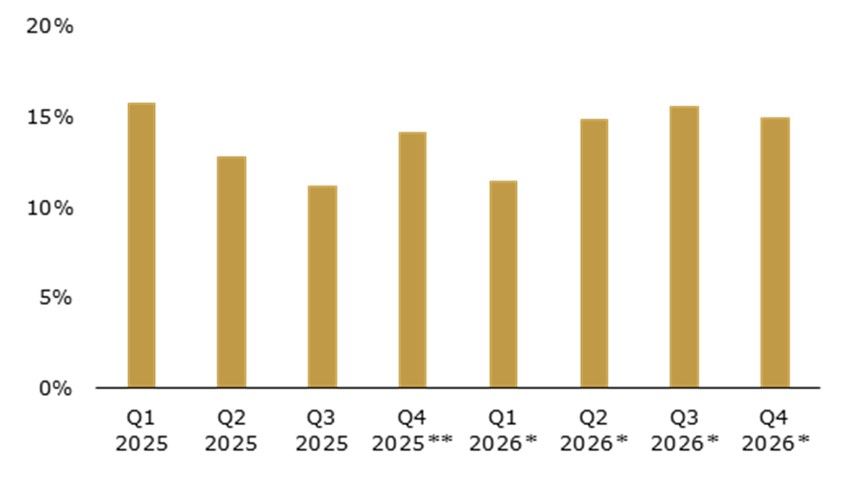

Analysts are expecting this excellent run to continue. Estimates for year-over-year earnings growth rates for all four quarters of 2026 are in double-digits, and for all of 2026, the S&P 500 is expected to grow earnings by nearly 15%.

S&P 500 Quarterly Year-over-Year Earnings Growth: 2025 actuals and 2026 estimates

* - estimates for 2026 earnings are from FactSet’s Earnings Insight. ** - blended earnings growth rate based on a combination of reported earnings numbers and estimate with 96% of companies reporting. Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and not subject to fees. It is not possible to invest directly in an index. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast or guarantee of futures results. Source: Kestra Investment Management with data from FactSet Earnings Insight and Bloomberg. Index: S&P 500. Data as of February 27, 2026.

Over the course of this earnings season, 73% of companies beat their earnings estimates, and the same number beat revenue estimates. While these rates are impressive, they are weaker relative to their ten-year averages. Those that beat, however, had earnings coming in 6.8% above estimates.

Earnings season reinforced that the state of the stock market remains strong. Robust growth rates in revenue, tailwinds from fiscal stimulus and monetary policy, and improving breadth all signal optimism that the rally can continue.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.