Higher Oil, Higher Stakes: A New Test for Consumers and the Fed

Higher Oil, Higher Stakes: A New Test for Consumers and the Fed

- Higher oil prices pressure consumers, but duration matters. Short-lived spikes typically slow spending only modestly; prolonged increases pose a greater risk to growth.

- Inflation becomes a problem if energy prices stay elevated. Temporary oil shocks lift headline inflation briefly, while sustained gains could delay Fed rate cuts.

- Volatility isn’t a strategy signal. Energy-driven market swings create near-term uncertainty, but diversified, long-term investors have historically been rewarded for staying disciplined.

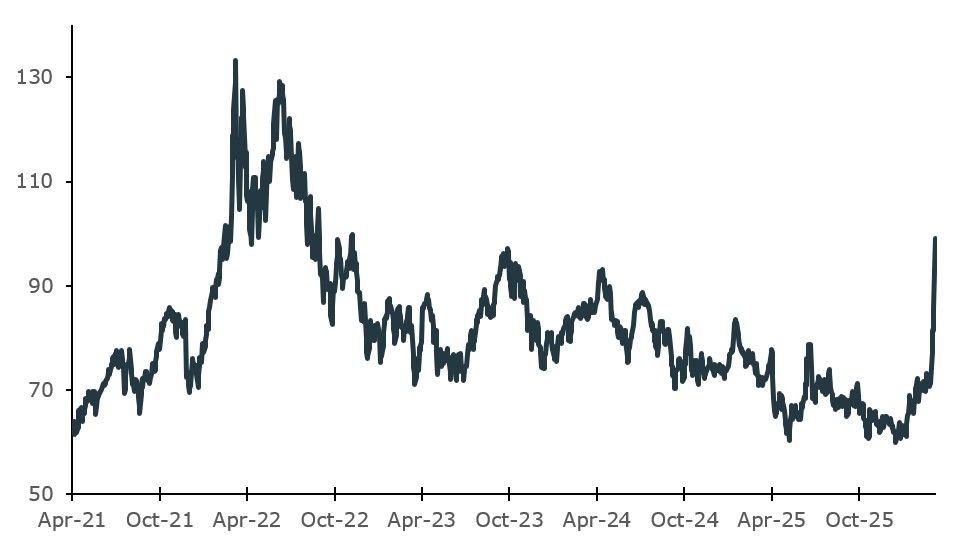

Brent Crude Oil Price ($/bbl)

Past performance is not a reliable indicator of current or future results. Source: Kestra Investment Management with data from FactSet. Time period from April 2021 – March 9, 2026.

For the U.S. consumer, higher oil prices act as a tax that limits how much consumers can spend on other items. Because the US economy is heavily dependent on consumers, higher oil prices represent a meaningful headwind to continued GDP growth. While pinpointing the exact economic impact of more expensive oil is difficult, one often-cited quote suggests that every $10 increase in the price of oil sets back economic growth by 0.1%. Other studies show that even the increase in the probability of supply shocks can have a similar drag on economic growth.

Even more important than the level of oil prices is the duration – how long do high prices remain? If oil prices fall back after a short spike, the effects on inflation and the economy are likely to fade quickly. Analysis by Piper Sandler shows that higher gasoline prices tend to push headline inflation up for a few months, but the impact does not meaningfully spill over into core inflation, which better reflects underlying price pressures. That’s because energy now makes up a much smaller share of household spending than it did decades ago. As a result, consumers generally absorb temporary increases at the pump without sharply cutting back elsewhere. In this scenario, any slowdown in consumer spending or economic growth would likely be modest and short‑lived, with little impact on jobs.

But that benign picture changes if oil prices stay elevated for an extended period. Piper Sandler estimates that every 15% rise in gasoline prices can add about half a percentage point to year‑over‑year headline inflation within a few months. Sustained increases gradually squeeze purchasing power and raise inflation readings for longer.

While the U.S. economy is more energy‑independent and resilient than in the past, limiting the risk of a major growth shock, persistently higher oil prices would still be inflationary and could weigh on spending and confidence over time. For investors, the key distinction is whether higher energy prices prove temporary noise or a lasting trend.

Cooling Inflation or Protecting Jobs? The Federal Reserve’s Dilemma

Another potential complication of higher oil prices is the Federal Reserve’s inability to respond. If elevated oil prices drove inflation higher, the Fed would normally raise interest rates, acting as a brake on the economy and tamping down prices. However, that playbook is more challenging because the other side of the Fed’s dual-mandate—maximum employment—is becoming more stressed.

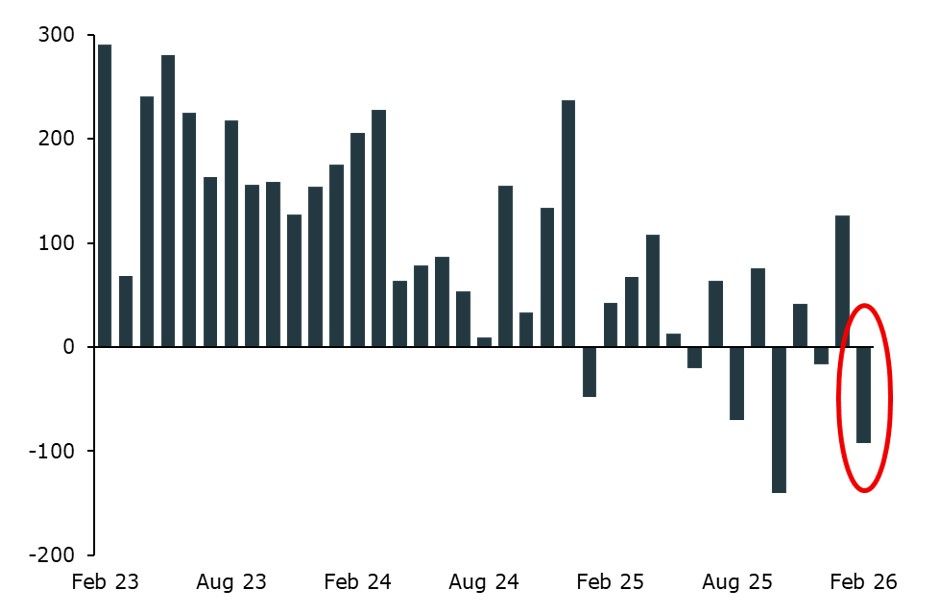

On March 6th the Bureau of Labor Statistics released their monthly payroll report, which showed an unexpected decrease of 92,000 jobs. It’s only the 6th time in 3 years with negative growth, but the expectation for February jobs was very different from reality. Every major bank and market researcher was predicting marginally positive job growth, so this report was a shock to market participants.

As of this writing, markets are still pricing in about two Fed funds rate cuts this year, which has been largely consistent in 2026 so far.

February Jobs Disappoint

Monthly Change in Non-Farm Payrolls (thousands)

Source: Kestra Investment Management, U.S. Bureau of Labor Statistics with data from Federal Reserve Bank of St. Louis. Data as of March 6, 2026.

A weakening labor market alongside rising oil prices and sustained inflation would make the Fed’s job markedly more difficult. Tightening monetary policy to tamp down inflation may strangle an already weak jobs market. Remaining accommodative risks headline inflation running away from them.

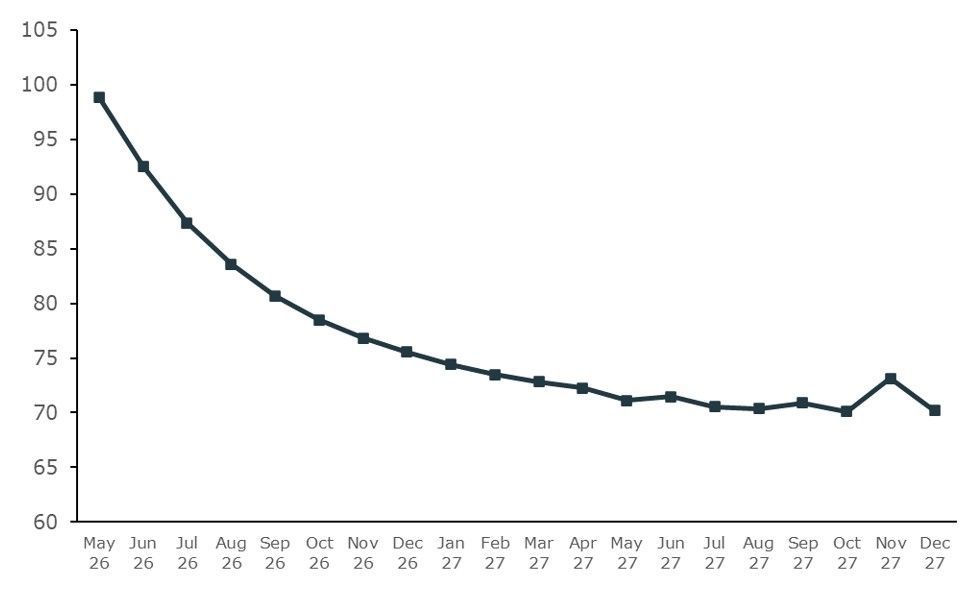

The good news for consumers is that the oil markets are expecting prices to ease in the latter part of the year. In fact, oil futures contracts suggest prices may drop below $90 by the summer, which would also suggest market participants expect the conflict to not be prolonged.

Brent Crude Continuous Futures Contracts ($/bbl)

Past performance is not a reliable indicator of current or future results. Forward looking estimates may not come to pass. Source: Kestra Investment Management with data from FactSet. Data as of March 6th, 2026.

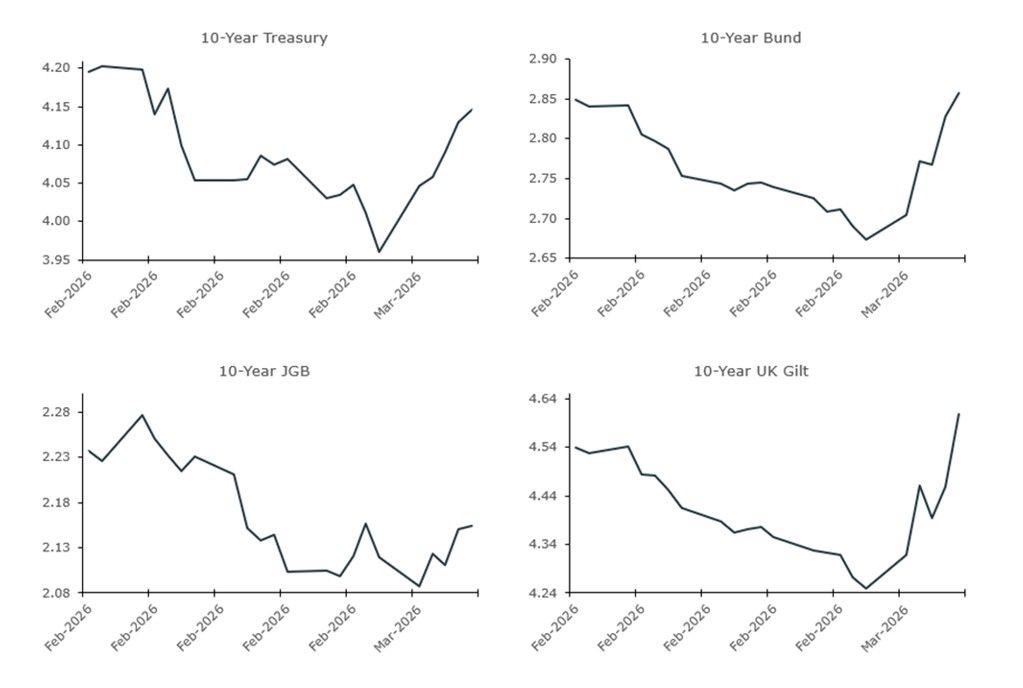

While the oil market appears to be betting that prices will not remain elevated, some corners of the fixed-income market are preparing for higher inflation. For instance, 10-year bond yields in the US, UK, Japan, and Germany are all trading higher since the conflict.

Global Yields Are Moving Higher

10-Year Yields for US, UK, Japanese, and German Bonds

Past performance is not a reliable indicator of current or future results. Source: Kestra Investment Management with data from FactSet. Data as of March 6th, 2026.

Conclusion

In addition to the very real human cost of conflict, higher oil prices introduce short‑term uncertainty for consumers, markets, and policymakers, especially when inflation and labor conditions are already somewhat precarious. Yet history offers an important reminder: periods of oil price volatility have often been followed by constructive opportunities for disciplined, long‑term investors. While sustained energy inflation can pressure spending and complicate the Fed’s response, markets have repeatedly shown an ability to adapt as growth drivers shift and a new equilibrium emerges. For investors, the takeaway is not to react to volatility itself, but to remain focused on fundamentals, diversification, and patience—traits that have historically been rewarded in the aftermath of energy‑driven market stress.

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.