Market Tensions and an IPO Comeback: What to Expect and Why it Matters

Kara Murphy

Market Tensions and an IPO Comeback: What to Expect and Why it Matters

Will this be the year the initial public offering (IPO) market finally gets its mojo back? After sinking in 2022, more companies have been indicating an interest in going public, encouraged by improving market conditions and renewed investor appetite for growth.

That said, the backdrop isn’t without complications. Recent market volatility tied to rising oil prices and escalating tensions in the Middle East is a reminder that the IPO window can open (and close) quickly. As such, expectations for a rebound in IPO activity come with an important caveat: timing will matter.

In this week’s Markets in a Minute, we explore the outlook for IPOs, the implications for investors and risks to the forecast.

Unicorns Take Flight

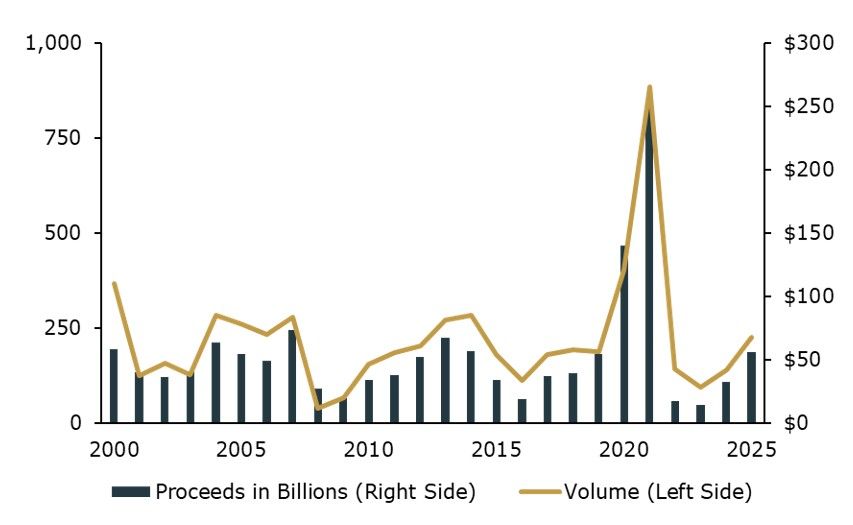

An estimated 200 to 230 companies could go public this year, potentially raising $40 to $60 billion, according to research from Renaissance Capital. That would bring activity closer to the 20-year average of roughly 250 IPOs annually. By comparison, just 71 companies went public in 2022, raising about $8 billion.

Other forecasts for this year are also bullish. Goldman Sachs , for instance, expects total IPO proceeds to quadruple to a record $160 billion. Software and healthcare companies are expected to account for the largest share of IPOs by number. However, offerings by a relatively small group of late-stage technology and artificial intelligence (AI) firms are likely to generate the lion’s share of total proceeds, according to the investment bank.

Among the highly valued, privately held billion-dollar companies (or so-called unicorns) expected to go public this year are Elon Musk’s SpaceX, artificial intelligence firm Anthropic, and ChatGPT maker OpenAI Group. By some accounts, SpaceX’s IPO could be the largest ever, potentially raising $30 billion, which would surpass the record set by Saudi Aramco in 2019.

U.S. IPO Activity: Volume and Total Proceeds (2000 to 2025)

Past performance is not a reliable indicator of current or future results. Source: Kestra Investment with data from the SEC. 2025 data is annualized based on the first three quarters of the number of U.S. IPOs and total proceeds.

The Upside of More IPOs

Why should investors cheer the return of a robust level of IPO activity?

For starters, IPO activity is a barometer of market health. When companies are confident enough to go public and investors respond favorably to their offerings, the dynamic signals confidence in the broader economy and, more specifically, the growth prospects of firms turning to the public markets for capital.

For investors, the anticipated wave of IPOs could also present some unique opportunities, including the chance to buy into relatively mature companies that have been off limits to the average retail investor.

Historically, companies went public when they were still fairly young because they needed access to lower-cost capital to hire, build factories and otherwise fund their growth. In recent years, however, companies have tended to stay private for longer because many have been able to access ample capital from private equity funds and private credit markets. Staying private for longer has also allowed companies to find their footing without the intense focus on quarterly results (or hefty regulatory burdens) that public companies face. In 2000, the median age for a company going public was 6 years old. By 2025, it had doubled to 12 years, according to a University of Florida study.

The anticipated pickup in IPO activity should also expand the opportunity set for investors seeking exposure to the AI revolution. Many of the companies that have benefitted most from the AI boom are still privately held, in part because, until recently, they haven’t needed vast amounts of capital to grow. As their capital needs increase and more of them enter the public sphere, a wider group of investors will have the chance to participate in their growth.

Risks to the Outlook

Of course, the year is still young, and a lot can happen. Just as the number of IPOs tends to rise when markets are on the upswing, the opposite is also true. More than once we’ve seen expectations for robust IPO activity upended by major events that made markets jittery and led companies to delay offerings, particularly those planning blockbuster IPOs.

A shift in investor sentiment towards industries expected to produce large numbers of IPOs can also put a damper on things. This year, for instance, investors have grown skittish about the potential impact of AI on software firms, driving down share prices in the industry and prompting speculation that some smaller tech companies may delay offerings until conditions improve.

Off to the Races

No doubt, the performance of early 2026 IPOs is being watched closely by investors, firms planning to go public later in the year and others seeking to gauge the market’s appetite for new listings.

It’s worth noting that the share prices of newly public companies tend to be more volatile than peers who have been public for longer. That’s especially true for highly anticipated IPOs that provide investors with exposure to industries that aren’t well-represented in the universe of publicly traded stocks. For instance, the share prices of companies generating a lot of buzz will surge when they first go public, fueled by pent-up demand, and then gradually settle to more-sustainable levels.

Even a poor public debut isn’t necessarily an indicator of a stock’s long-term prospects. Keep in mind that Google, which was a well-known brand when it went public in 2004, had a disappointing IPO but went on to deliver stellar returns over time.

Of course, whether the IPO market ultimately regains its footing will depend not just on company fundamentals, but on the broader market environment. Periods of heightened volatility—such as those driven by geopolitical conflict or sharp moves in energy prices—have a history of delaying IPOs rather than canceling them outright.

For investors, that distinction matters. A slower or more uneven IPO calendar doesn’t eliminate opportunity, but it does raise the bar for selectivity, patience and diversification. As always, navigating new listings is less about chasing headlines and more about staying disciplined and focused on long‑term goals.

Invest wisely and live richly,

Kara

The opinions expressed in this commentary are those of the author and may not necessarily reflect those held by Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC. The material is for informational purposes only. It represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. It is not guaranteed by any entity for accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation. Kestra Advisor Services Holdings C, Inc., d/b/a Kestra Holdings, and its subsidiaries, including, but not limited to, Kestra Advisory Services, LLC, Kestra Investment Services, LLC, and Bluespring Wealth Partners, LLC, do not offer tax or legal advice.